python用yfinance抓取数据

yfinance是利用雅虎财经的数据模块,可以作为一个用python分析美股的数据来源。

这是一篇python使用yfinance最新教程2024,熟悉一下yfinance的基本功能。下面主体内容是摘自这篇文章。

使用需要的库:

- ython >= 2.7, 3.4+

- Pandas (tested to work with >=0.23.1)

- Numpy >= 1.11.1

- requests >= 2.14.2

- lxml >= 4.5.1

- pandas_datareader >= 0.4.0

yfinance模块介绍

yfinance的几大功能块:

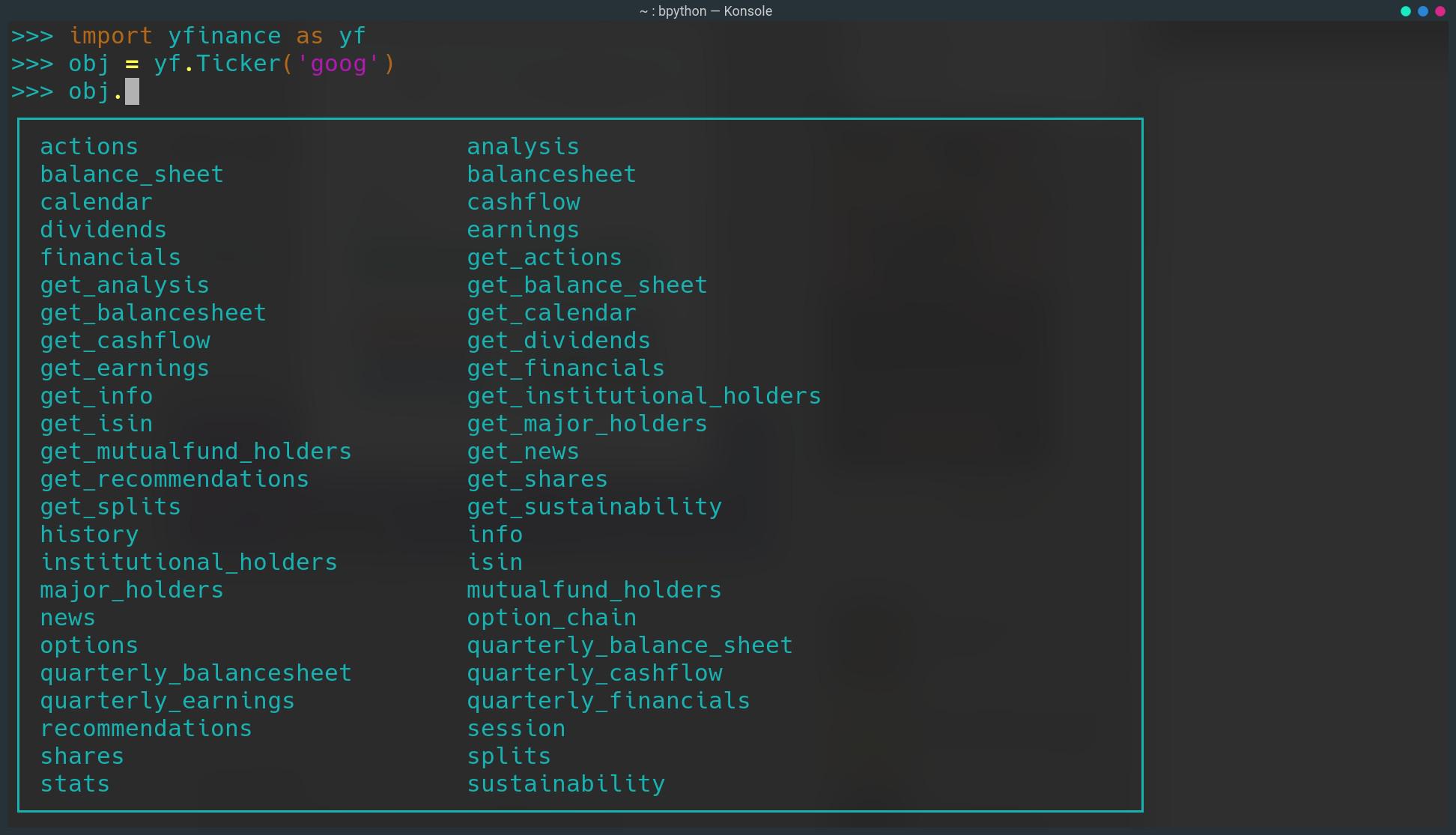

Ticker

yfinance下ticker获取资料方式:

获取单只股票历史数据:

def history(self, period="1mo", interval="1d",

start=None, end=None, prepost=False, actions=True,

auto_adjust=True, back_adjust=False,

proxy=None, rounding=False, tz=None, timeout=None, **kwargs):

"""

:Parameters:

period : str

Valid periods: 1d,5d,1mo,3mo,6mo,1y,2y,5y,10y,ytd,max

Either Use period parameter or use start and end

interval : str

Valid intervals: 1m,2m,5m,15m,30m,60m,90m,1h,1d,5d,1wk,1mo,3mo

Intraday data cannot extend last 60 days

start: str

Download start date string (YYYY-MM-DD) or _datetime.

Default is 1900-01-01

end: str

Download end date string (YYYY-MM-DD) or _datetime.

Default is now

prepost : bool

Include Pre and Post market data in results?

Default is False

auto_adjust: bool

Adjust all OHLC automatically? Default is True

back_adjust: bool

Back-adjusted data to mimic true historical prices

proxy: str

Optional. Proxy server URL scheme. Default is None

rounding: bool

Round values to 2 decimal places?

Optional. Default is False = precision suggested by Yahoo!

tz: str

Optional timezone locale for dates.

(default data is returned as non-localized dates)

timeout: None or float

If not None stops waiting for a response after given number of

seconds. (Can also be a fraction of a second e.g. 0.01)

Default is None.

**kwargs: dict

debug: bool

Optional. If passed as False, will suppress

error message printing to console.

"""

举例:

data = goog.history(interval='1m', start='2022-01-03', end='2022-01-10')

data.head()

下载多只股票历史数据:

def download(tickers, start=None, end=None, actions=False, threads=True,

group_by='column', auto_adjust=False, back_adjust=False,

progress=True, period="max", show_errors=True, interval="1d", prepost=False,

proxy=None, rounding=False, timeout=None, **kwargs):

"""Download yahoo tickers

:Parameters:

tickers : str, list

List of tickers to download

period : str

Valid periods: 1d,5d,1mo,3mo,6mo,1y,2y,5y,10y,ytd,max

Either Use period parameter or use start and end

interval : str

Valid intervals: 1m,2m,5m,15m,30m,60m,90m,1h,1d,5d,1wk,1mo,3mo

Intraday data cannot extend last 60 days

start: str

Download start date string (YYYY-MM-DD) or _datetime.

Default is 1900-01-01

end: str

Download end date string (YYYY-MM-DD) or _datetime.

Default is now

group_by : str

Group by 'ticker' or 'column' (default)

prepost : bool

Include Pre and Post market data in results?

Default is False

auto_adjust: bool

Adjust all OHLC automatically? Default is False

actions: bool

Download dividend + stock splits data. Default is False

threads: bool / int

How many threads to use for mass downloading. Default is True

proxy: str

Optional. Proxy server URL scheme. Default is None

rounding: bool

Optional. Round values to 2 decimal places?

show_errors: bool

Optional. Doesn't print errors if True

timeout: None or float

If not None stops waiting for a response after given number of

seconds. (Can also be a fraction of a second e.g. 0.01)

"""

举例:

data = yf.download(['GOOG','META'], period='1mo')

data.head()

把上面下载数据group一下:

data = yf.download(['GOOG','META'], start='2021-12-10', end='2021-12-30', group_by='ticker')

data.head()

获取基本面信息:

基本面信息范畴有:

举例:

dhr = yf.Ticker('DHR')

info = dhr.info

info.keys()

info['sector']

'Healthcare'

dhr.earnings

dhr.get_financials()

pnl = dhr.financials

bs = dhr.balancesheet

cf = dhr.cashflow

fs = pd.concat([pnl,bs,cf])

print(fs)

fs.T

由于没有一次下载多个股票基本面信息的方式,所以要用loop去获取。

tickers = ['FB','AMZN','NFLX','GOOG']

tickers

tickers = [yf.Ticker(ticker) for ticker in fang]

[yfinance.Ticker object <FB>,

yfinance.Ticker object <AMZN>,

yfinance.Ticker object <NFLX>,

yfinance.Ticker object <GOOG>]

dfs = [] # list for each ticker's dataframe

for ticker in tickers:

# get each financial statement

pnl = ticker.financials

bs = ticker.balancesheet

cf = ticker.cashflow

# concatenate into one dataframe

fs = pd.concat([pnl, bs, cf])

# make dataframe format nicer

# Swap dates and columns

data = fs.T

# reset index (date) into a column

data = data.reset_index()

# Rename old index from '' to Date

data.columns = ['Date', *data.columns[1:]]

# Add ticker to dataframe

data['Ticker'] = ticker.ticker

dfs.append(data)

data.iloc[:,:3]# for display purposes

整理数据:

parser = pd.io.parsers.base_parser.ParserBase({'usecols': None})

for df in dfs:

df.columns = parser._maybe_dedup_names(df.columns)

df = pd.concat(dfs, ignore_index=True)

df = df.set_index(['Ticker','Date'])

df.iloc[:,:5] # for display purposes

获取期权数据:

使用Ticker.options和Ticker.option_chain方式:

分别给出下面信息:

分别给出下面信息:

- options 返回到期日信息。

- option_chain 返回期权链信息。

期权链包括:

举例(获得call/put信息):

calls = options.calls

calls

puts = options.puts

puts

获取机构持股信息

aapl.insitutional_holders

数据提供商

Nasdaq数据提供商。。。。。这里有一篇Nsadaq DATA Link API使用教程。

polygon.io数据的免费版提供5个查询。提供将顶级REST和流式股票市场API的强大功能无缝数据集成。。。。。这里有一篇Polygon API使用教程。

Alpaca Markets数据提供商,也有免费版,15分钟延迟。。。。。。这里有一篇Alpaca Market API使用教程。

额外信息

-

一个金融数据分析博客。。。找到这博客是因为搜索option greek找出来期权交易这篇文章。

注:会继续更新

留下评论